Eleven million Capital One debit cards had to move to the Discover Network by Q4 2025. I designed the servicing experience for the customers who could not finish that journey alone.

Capital One was reissuing 11 million existing debit cards onto the Discover Network. On-file and wallet spend made up 60% of $60B in total debit spend, and that volume is hit hardest whenever cards are replaced.

The business needed a conversion that was fast and low-friction, while protecting purchase volume that often drops during reissues because customers struggle to update payment methods to the new card.

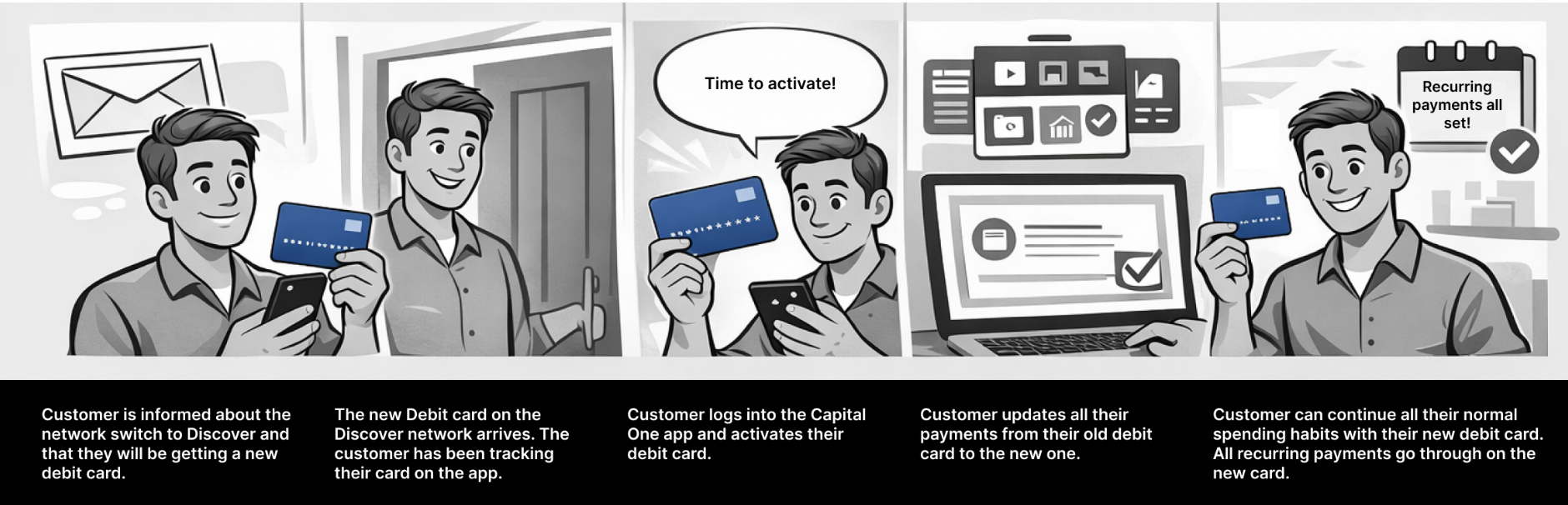

A mass debit reissue at this scale is unprecedented, and many customers assume the worst when a new card arrives unprompted. Most only expect to activate it. Updating recurring payments is the real pain point, and it is often where people switch spend to another method or bank.

Lower-income, heavy debit users face the highest risk: a missed payment can turn into rent, utilities, or payroll disruption, not just inconvenience.

If we designed a multi-channel, guided experience focused on activation and updating cards on file, we could minimize customer disruption and reduce purchase volume loss. Automation and clear guidance through a process customers otherwise experience as disruptive and effortful would make them more likely to activate and reconnect the payments that keep spend on Capital One.

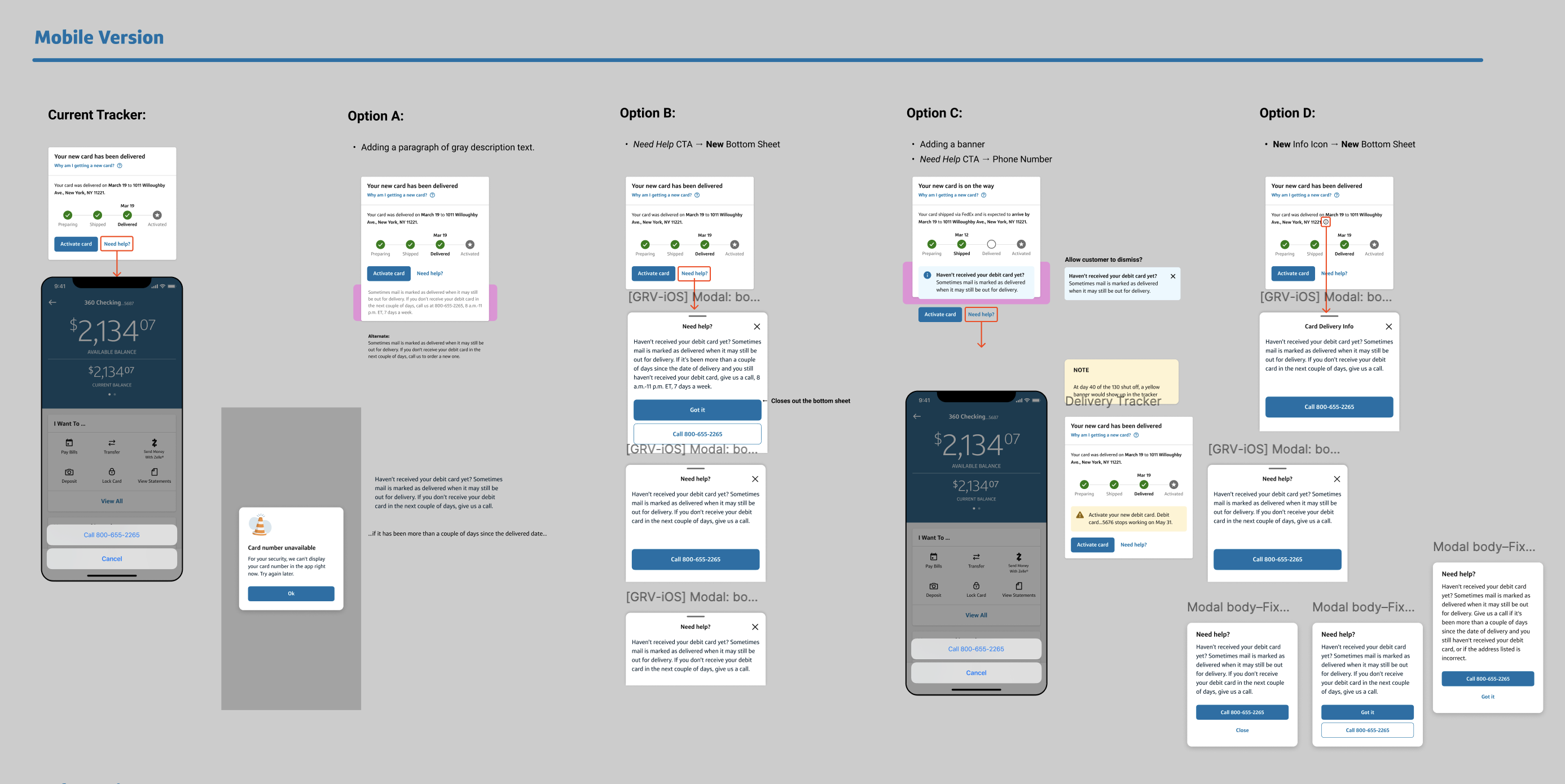

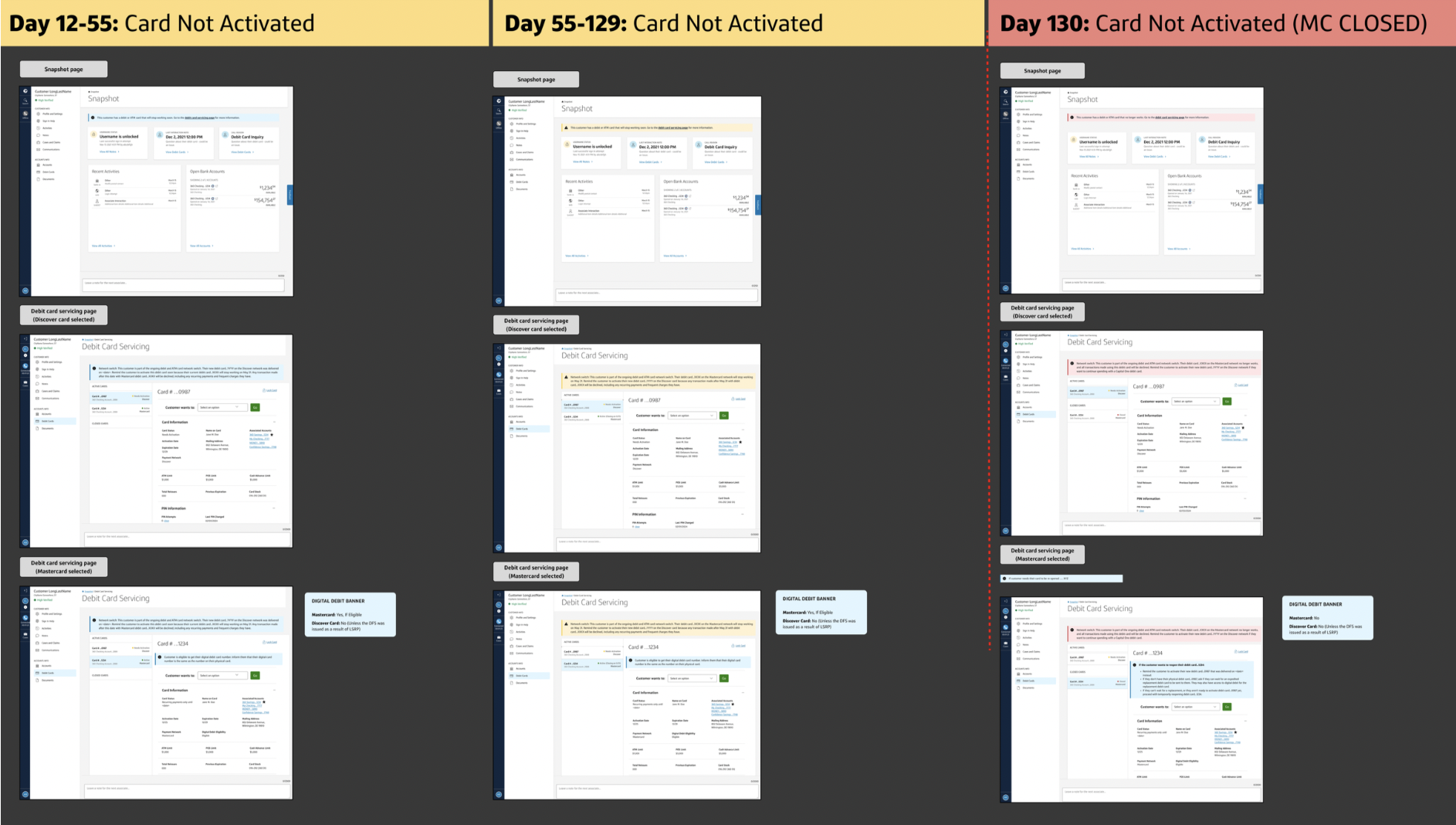

I owned the servicing side of conversion: the experience for customers who never complete the happy path and land with an associate instead. Servicing is already the edge case of a migration this large. I designed the edge case of that edge case, including lost or stolen cards mid-conversion, state-aware guidance, and the tooling associates needed to resolve it without losing the customer or the spend.

I shipped an in-app tracker with state-aware help, associate tools for lost or stolen cards mid-conversion, and a risk-constrained way to briefly reactivate the old card when access could not lapse.

As a result, activation reached 73.25%, all cards have been converted, and as of Q1 2026 we are nearing $30B in purchase volume on converted cards, more than halfway to the $55B target.